If you manufacture or process goods, whether you run a bakery in Westlands, a juice factory along Thika Road, or a packaging business in Mombasa, your ability to price correctly and stay profitable starts with one thing: understanding your true production costs. Yet for most Kenyan SME manufacturers, production costing is either done on gut feel, a rough spreadsheet, or not at all. That gap between what things feel like they cost and what they actually cost is where margins disappear.

Kenya’s manufacturing sector is growing contributing 7.8% to GDP and generating over 352,000 direct jobs and SMEs are the engine powering that growth. But SMEs make up 98% of all businesses in Kenya while contributing only a fraction of total manufacturing output. One reason for that gap is operational businesses that can’t accurately cost their products can’t scale them. This guide breaks down production costing in plain language, with practical examples grounded in the Kenyan business context.

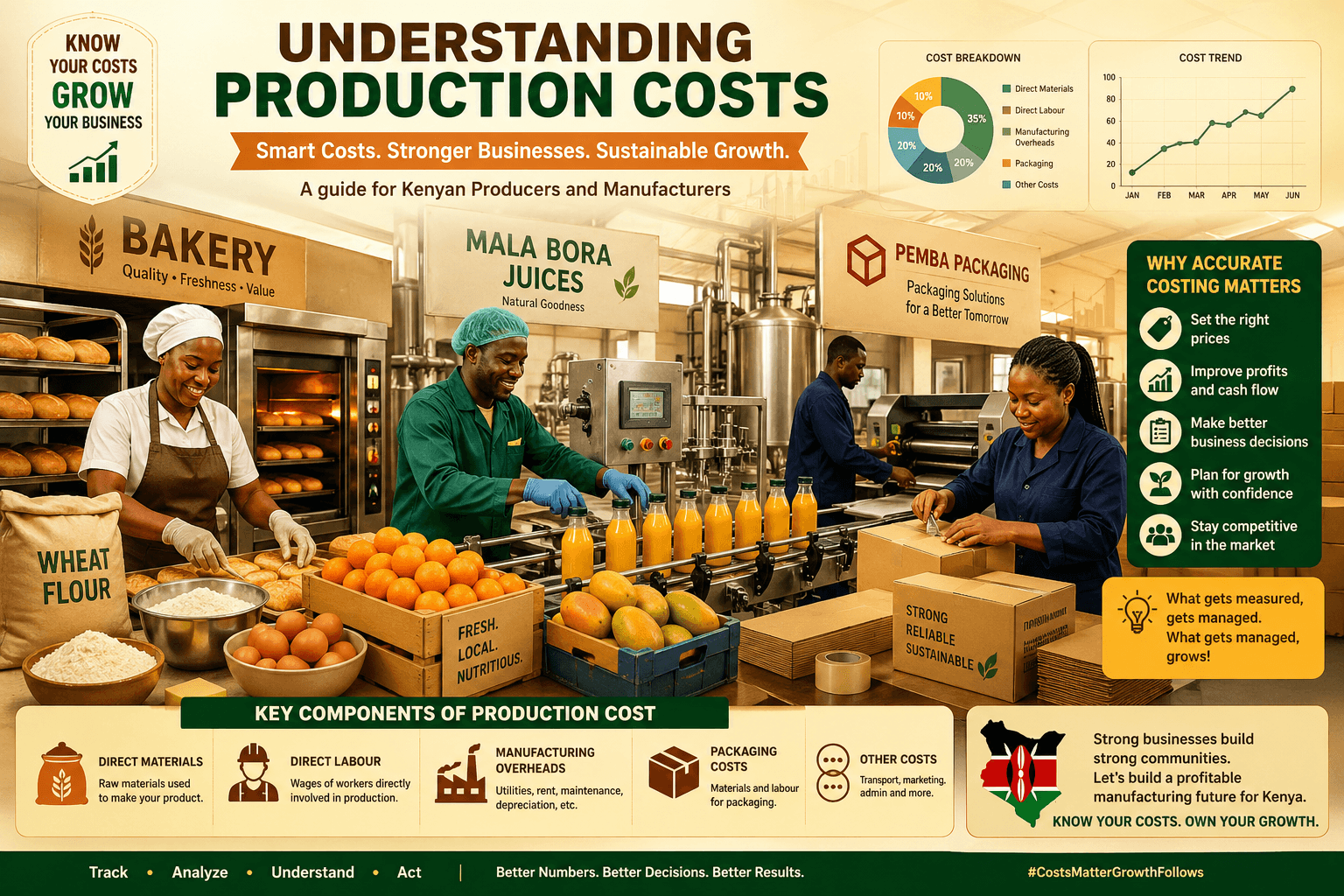

What Are Production Costs, and Why Do They Matter?

Production costs are every expense that goes into making a finished product from the raw ingredients you buy, to the electricity powering your machines, to the wages of the people on your production floor. Product costs are grouped into three core categories: direct materials, direct labour, and manufacturing overhead. Together, these three elements make up your total cost per unit the number that determines whether you’re pricing to profit or pricing to loss.

Here’s why this matters in the Kenyan context: rising input costs fuel, packaging, flour, cooking gas are squeezing margins across the food production and FMCG sectors. If you don’t know your exact production cost, you cannot respond to input price changes intelligently. You either absorb the loss silently or reprice blindly and risk losing customers.

The Three Pillars of Production Costing

1. Direct Materials — Your Bill of Materials (BOM)

Direct materials are the raw inputs that physically become part of your finished product. For a mandazi bakery, it’s flour, sugar, oil, and eggs. For a juice manufacturer, it’s fruit, water, preservatives, and bottles. A Bill of Materials (BOM) is essentially the recipe, a comprehensive list of all materials, quantities, and their associated costs required to produce one unit of your product.

Getting your BOM right is the foundation of everything else. Each ingredient needs to be recorded at the correct unit of measure (grams, litres, kilograms) and at the actual purchase cost, not an estimate. The quantity formula is straightforward:

Total Ingredient Qty = (Units per pack × Number of packs) + Loose/fractional quantityFor example: a recipe needs 500 g of wheat flour, but you buy flour in 50 kg bags. Your BOM records 500 g against the cost-per-gram derived from the 50 kg bag price. Consistency in unit conversions prevents the most common costing errors and in a production environment, small per-unit errors multiply fast across hundreds or thousands of units.

The total direct material cost is calculated as:

Direct Materials Cost = Beginning Raw Materials Inventory + Purchases − Ending Raw Materials Inventory2. Direct Labour — The Human Cost of Production

Direct labour is the cost of staff who are physically involved in making the product the person mixing dough, operating the filling machine, or assembling goods on the line. Direct labour includes wages, benefits, and any payroll taxes directly attributable to production staff.

In a Kenyan SME setting, many production staff are casual workers paid on a daily or piece-rate basis — which can make labour costs variable and easy to overlook in costing models. The key is to calculate labour cost per production batch: how many labour-hours does one batch take, and what is the total wage cost for that time? That per-batch labour cost then divides across all units produced in the batch to give you a per-unit labour contribution.

3. Manufacturing Overheads — The Costs That Hide in Plain Sight

Overheads are where most Kenyan manufacturers get stuck. They’re real costs — but they don’t sit on a single product the way flour does. Manufacturing overhead includes all indirect production expenses not explicitly tied to specific products — equipment depreciation, rent, insurance, and utilities.

Overheads typically fall into three types:

- Fixed overheads — costs that stay constant regardless of how much you produce. Kitchen rent, equipment lease payments, a permanent factory security guard. Whether you produce 100 units or 1,000, the rent is the same.

- Variable overheads — costs that rise and fall with production volume. Electricity consumption for machinery, cooking gas, packaging materials. Variable overheads change with shifts in production volume — the more you produce, the higher these costs go.

- Percentage-based overheads — overheads calculated as a percentage of total raw material cost. For example, a logistics allowance set at 3% of ingredient cost, or a wastage buffer of 2%.

Common overhead items for a Kenyan food producer or manufacturer include:

- Electricity (KPLC bills — a significant and often unpredictable overhead)

- Cooking gas or LPG

- Water

- Kitchen or factory rent

- Equipment maintenance and repairs

- Cleaning and sanitation supplies

- Packaging materials not captured in the BOM

- Kitchen staff wages for non-production roles (supervisors, cleaning crew)

- Administrative costs allocated to the production centre

Overhead costs should be allocated based on the percentage of production time or space used for each product — so if you produce two product lines sharing one kitchen, you split overhead proportionally between them.

The Full Production Cost Formula

Once you have all three components, the formula is straightforward:

Total Unit Cost = Direct Materials Cost + Direct Labour Cost + Manufacturing Overhead CostLet’s make this real. Say you run a small nut butter production line in Nairobi:

| Cost Component | Detail | Amount (KES) |

|---|---|---|

| Direct materials | Macadamia nuts, oil, salt, jars, labels | 8,400 |

| Direct labour | 2 workers × 4 hrs × KES 200/hr | 1,600 |

| Overheads | Electricity, gas, cleaning, rent allocation | 1,200 |

| Total batch cost | 80 jars produced | 11,200 |

| Unit production cost | KES 11,200 ÷ 80 jars | KES 140 / jar |

With KES 140 as your floor cost, you can confidently set a retail price that covers cost, allows for distribution margin, and leaves you with profit. Without this calculation, many business owners price at KES 150 “because it feels right” — not knowing whether they’re making KES 10 margin or running a KES 5 loss after overheads.

From Recipe to Stock: The Production Lifecycle in a Managed System

In an informal or spreadsheet-based operation, costing calculations are done once — at setup — and then drift out of date as input prices change. A proper production management system ties costing to live inventory data through a structured lifecycle:

- Recipe / BOM Configuration — each finished good is configured with its ingredient list and overhead assignments. The system computes unit cost automatically: unit cost = sum of ingredient costs + sum of overhead costs.

- Materials Requisition (MRQ) — before a production run, a materials requisition is raised. The system explodes the recipe and calculates exactly how much of each raw material is needed for the planned production quantity.

- Approval — the requisition is reviewed and approved by an authorised person before raw materials are released — creating a control checkpoint that prevents unauthorised production.

- Raw Material Issuance — approved materials are issued out of inventory to the production centre, reducing stock balances in real time.

- Finished Goods Receipt — completed goods are received back into inventory, valued at the pre-computed unit cost (ingredients + overheads). The batch is closed.

This lifecycle closes the loop between production activity and inventory accuracy — so your stock reports reflect what’s actually in your warehouse, and your cost of goods sold is correctly computed rather than estimated.

Why Most Kenyan SME Producers Undercount Their Costs

There are predictable patterns in how production costs get undercounted. Recognising them is the first step to fixing them:

- Overheads are not assigned to products. Electricity, gas, and rent are paid as business expenses but never allocated to individual products. The cost is real — it’s just invisible in the product price.

- Ingredient quantities are approximated. When a recipe says “a handful of salt” or “about 2 kg of flour,” costing accuracy is gone. Precise grams and litres matter.

- Wastage and yield loss is ignored. Raw material yields are rarely 100%. Peeling, trimming, evaporation, and spoilage reduce the amount of usable input. A 1 kg orange yields roughly 400–500 ml of juice — the cost of the wasted 50–60% of the fruit must still be costed into that juice.

- Labour is treated as a fixed business cost, not a per-product cost. Staff wages are paid whether production runs or not — but they should still be allocated to what was produced during paid production hours.

- Input prices are not updated after supplier price changes. Costing models built six months ago with old commodity prices are actively misleading.

Research on Kenyan manufacturing SMEs shows a positive correlation between adopting structured operational technology and improved production efficiency and competitiveness — confirming that the gap between informal and formalised production management is a performance gap, not just an administrative one.

Fixed vs. Variable Overheads: Why the Distinction Matters for Pricing

Understanding whether an overhead is fixed or variable changes how you use it in pricing decisions. Manufacturing overhead must be divided up and allocated to each unit produced — but the method of allocation differs by cost type.

Fixed overheads get cheaper per unit as you produce more. If your monthly kitchen rent is KES 30,000 and you produce 1,000 units, rent contributes KES 30 per unit. If you scale to 3,000 units, it drops to KES 10 per unit. This is why volume matters so much to production profitability — fixed costs spread over more units dramatically improves your margin per unit.

Variable overheads stay roughly constant per unit regardless of scale. Electricity per unit doesn’t drop just because you’re producing more — you’re still consuming proportionally the same power per unit of output.

This distinction matters for pricing decisions: if a customer wants a bulk order at a lower price, you can offer a discount on the fixed overhead portion — not on the variable materials and direct labour portion, which are irreducible.

How PawaPOS Handles Production Costing End-to-End

PawaPOS includes a built-in production management module designed for exactly the kind of businesses described in this article — Kenyan producers in food processing, beverages, packaging, and light manufacturing who need structured costing without the complexity of enterprise manufacturing software.

Here’s how the module works in practice:

- Overhead Master — you define overhead types (Utilities, Labour, Packaging) and individual overhead items with their cost type: fixed amount, variable per-unit rate, or percentage of raw material cost. Pre-configured overhead templates include Electricity, Water, Gas, Kitchen Staff Wages, Kitchen Rent, Equipment Maintenance, Cleaning Supplies, and Packaging Materials.

- Stock Catalog with Bill of Materials — each finished product is configured with a full ingredient list. Each ingredient line captures the raw material, quantity in the correct unit of measure, packing conversion ratios, and unit cost. The system computes line costs (excl. VAT and incl. VAT) automatically.

- Computed Unit Cost — unit cost is automatically calculated as the sum of all ingredient costs plus all overhead costs. This becomes the valuation rate when finished goods are received back into inventory — ensuring your stock is always valued at true production cost.

- Materials Requisition with Recipe Explosion — when you initiate a production run, PawaPOS explodes the recipe automatically across the planned quantity and generates a materials requisition with exact raw material requirements.

- Approval Controls — production batches require approval before materials can be released, giving management a control checkpoint over production activity.

- Raw Material Issuance & Finished Goods Receipt — raw materials are issued from stock (reducing inventory) and finished goods are received into stock (increasing inventory at computed unit cost) — keeping inventory balances accurate throughout the production cycle.

The result: your stock reports, cost of goods sold, and profitability figures all reflect actual production reality — not estimates. You can answer the question “what does it cost me to make this?” with a number, not a guess. Learn more on the CosmoPawa website or read our related guide on managing inventory shrinkage in Kenyan retail businesses.

Free consultation

Ready to see PawaPOS in action?

Chat with our team on WhatsApp — we’ll walk you through a live demo at your convenience.

Typically replies within minutes

Final Thoughts

Production costing is not an accounting exercise — it’s a survival skill for any Kenyan manufacturer. Knowing your true unit cost gives you the confidence to price correctly, negotiate with distributors, respond to input cost increases, and make volume decisions intelligently. Kenya’s manufacturing growth ambitions depend on SMEs becoming more operationally sophisticated — and costing discipline is where that sophistication begins.

Whether you’re running a single production line or managing multiple production centres across branches, the principle is the same: every cost that goes into making your product must be tracked, assigned, and computed — not guessed. The businesses that know their numbers are the ones that survive input price shocks, scale profitably, and build brands that last. Chat with us on WhatsApp at +254 710 901 965 to see how PawaPOS can bring this structure to your production operation.